Company Match: What It Is and How It Impacts Your Business

Discover how company match programs work, their impact on recruitment, and strategies to maximize this benefit for both employers and employees in 2026.

Apr 19, 2026

scheduled

Understanding the company match concept is essential for business owners who want to attract and retain top talent in today's competitive marketplace. A company match represents one of the most powerful tools employers can leverage to demonstrate their commitment to employee financial wellbeing while simultaneously building a more stable, loyal workforce. For high-ticket businesses selling products or services over $2,500, particularly those operating through digital channels, offering competitive benefits like a company match can be the difference between securing elite sales professionals and watching them join competitors.

Understanding Company Match Fundamentals

The company match primarily refers to employer contributions to retirement plans, specifically 401(k) accounts, where companies match a percentage of what employees contribute. Charles Schwab offers insights into how 401(k) matching functions, explaining that employers typically match between 50% and 100% of employee contributions up to a certain percentage of their salary.

The most common company match formula follows a 50% match on the first 6% of employee contributions, though formulas vary widely across industries and organizations. Some companies offer dollar-for-dollar matches up to 3% or 4%, while more generous employers might match 100% of contributions up to 6% or even higher.

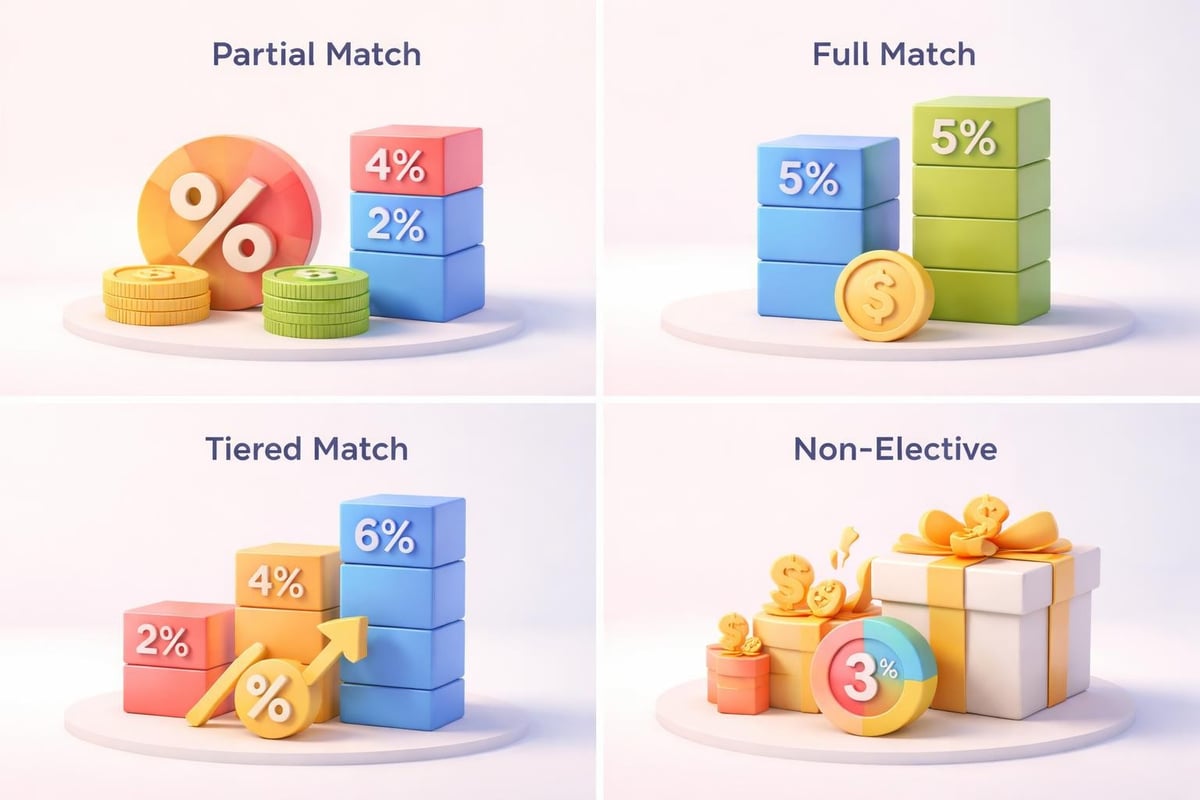

Common Company Match Structures

Different businesses structure their company match programs based on budget constraints, industry standards, and talent acquisition goals. Here are the primary matching structures:

Partial match: Employer matches 50% of employee contributions up to a specified percentage

Full match: Dollar-for-dollar matching up to a predetermined limit

Tiered match: Different matching percentages at different contribution levels

Non-elective contributions: Employer contributes regardless of employee participation

Understanding these structures helps businesses design competitive packages that appeal to high-ticket sales professionals who expect comprehensive benefits as part of their compensation.

The Financial Impact of Company Match Programs

According to Fidelity's research on average 401(k) matches, the typical employer match was approximately 4.7% of employee compensation in recent years. This seemingly modest percentage translates into substantial long-term wealth accumulation when considering compound growth over decades.

Consider an employee earning $75,000 annually who contributes 6% of their salary ($4,500) with a company match of 50% on that 6% ($2,250). Over 30 years with average market returns, this "free money" from the employer could grow to represent hundreds of thousands of dollars in retirement savings.

Match Formula | Employee Contribution | Employer Contribution | Total Annual Addition |

|---|---|---|---|

50% up to 6% | $4,500 (6%) | $2,250 | $6,750 |

100% up to 3% | $4,500 (6%) | $2,250 | $6,750 |

100% up to 6% | $4,500 (6%) | $4,500 | $9,000 |

50% up to 8% | $6,000 (8%) | $3,000 | $9,000 |

Based on $75,000 annual salary

The company match serves as immediate return on investment for employees, effectively guaranteeing returns that far exceed what any investment vehicle could promise. This makes participation in employer-sponsored retirement plans with matching contributions one of the most fundamental financial planning strategies.

Vesting Schedules and Their Implications

Many company match programs include vesting schedules that determine when employees gain full ownership of employer contributions. Bankrate explains vesting concepts, noting that immediate vesting grants employees instant ownership, while graded or cliff vesting schedules require tenure before employees fully own matched funds.

Common vesting approaches include:

Immediate vesting (employee owns 100% immediately)

Cliff vesting (0% until specific anniversary, then 100%)

Graded vesting (percentage increases annually until fully vested)

Understanding vesting schedules is particularly relevant for sales recruitment firms when evaluating compensation packages for candidates. A generous match with a six-year vesting schedule may be less attractive than a modest match with immediate vesting, especially for sales professionals who often move between opportunities.

Strategic Value for Employers

The company match provides substantial strategic advantages beyond employee satisfaction. Businesses that offer competitive matching programs typically experience lower turnover rates, higher employee engagement, and improved recruitment outcomes.

The Motley Fool's comprehensive guide emphasizes that employer matching contributions help companies compete for talent in tight labor markets. For businesses focused on building robust sales departments, offering a strong company match signals financial stability and long-term thinking.

Recruitment and Retention Benefits

High-performing sales professionals evaluate total compensation packages, not just base salary and commission structures. A competitive company match demonstrates that an organization values employee financial security and is willing to invest in their future.

When businesses are ready to hire top-tier sales talent, the presence or absence of a company match can influence candidate decisions. Sales professionals who excel in high-ticket environments often possess the financial acumen to recognize the long-term value of matching contributions.

Maximizing Company Match as an Employee

Employees should view failing to capture the full company match as leaving money on the table. Britannica Money explores strategies for contributions beyond employer match, but the foundational principle remains contributing enough to receive the maximum employer contribution.

For sales professionals working on commission structures, managing 401(k) contributions can be more complex due to variable income. However, the company match remains equally valuable regardless of how compensation is structured.

Steps to maximize your company match:

Determine your employer's matching formula - Review plan documents to understand exact matching percentages

Calculate minimum contribution required - Identify the contribution level that captures full match

Adjust contributions during enrollment - Set percentage high enough to maximize matching

Review annually - Ensure contribution rates still capture full match as salary changes

Consider contribution timing - Some matches are based on per-pay-period contributions

Many employees mistakenly believe they can "catch up" later in the year, but some company match programs only match per-pay-period contributions. Contributing $500 in December doesn't generate the same match as contributing smaller amounts throughout twelve months under certain plan structures.

When Company Match Isn't Available

Kiplinger examines whether 401(k) plans without employer matching remain worthwhile, concluding that tax advantages still make participation valuable even without matching. However, the absence of a company match significantly reduces the attractiveness of these plans compared to other retirement savings vehicles.

For businesses that cannot afford traditional company match programs, alternative benefit structures might include profit-sharing arrangements, non-elective contributions, or enhanced compensation in other forms.

Industry Benchmarks and Competitive Analysis

According to Kiplinger's analysis of average 401(k) matches, some of the most generous employers offer matches exceeding 6% of employee compensation, with a few organizations providing dollar-for-dollar matches on contributions up to 10% or more.

Industry variation is significant, with professional services firms, technology companies, and financial institutions typically offering more generous company match programs than retail or hospitality businesses. For companies in the sales recruitment space, understanding these benchmarks helps in properly positioning opportunities with vetted candidates.

Industry | Average Match | Typical Formula |

|---|---|---|

Professional Services | 5.2% | 100% up to 4%, 50% up to 6% |

Technology | 5.5% | Various, often generous |

Healthcare | 4.3% | 50% up to 6% |

Manufacturing | 4.8% | 50% up to 6% |

Retail | 3.2% | Varies widely |

Industry averages approximate based on multiple sources

Businesses competing for elite remote high-ticket sales talent should benchmark their company match against industry leaders rather than industry averages. Top performers expect top-tier benefits.

Tax Advantages and Contribution Limits

The company match provides immediate value, but understanding the broader tax context helps maximize benefits. Employee contributions to traditional 401(k) plans reduce taxable income in the contribution year, while employer matching contributions don't count toward the employee contribution limit.

CNBC Select outlines 401(k) employer matching mechanics, noting that 2026 contribution limits for employees under 50 are $23,000, while the total contribution limit combining employee and employer contributions reaches $69,000.

This means a company match doesn't reduce the amount employees can personally contribute. An employee can contribute the full $23,000 while also receiving thousands in employer matching contributions, all within legal limits.

Pre-Tax Versus Roth Considerations

Some employers offer company match on both traditional pre-tax and Roth 401(k) contributions, though the employer matching contribution itself is always made on a pre-tax basis regardless of how the employee designates their own contributions.

Understanding these distinctions becomes particularly important for high-income sales professionals in high-ticket closer roles who may be evaluating tax strategies across multiple income levels.

Designing Effective Company Match Programs

Business owners establishing or evaluating company match programs should balance several competing priorities: attracting talent, managing costs, encouraging participation, and maintaining financial flexibility.

Guideline discusses what constitutes a good 401(k) match and how matching contributions aid in recruiting and retaining talent. The research indicates that even modest matching programs significantly increase employee satisfaction and perceived value of total compensation.

Key considerations when designing a company match:

Budget constraints - Determine sustainable contribution levels based on profit margins

Competitive positioning - Research industry standards and direct competitor offerings

Participation goals - Structure matching to encourage broad employee participation

Vesting strategy - Balance retention incentives with employee fairness

Administrative complexity - Consider operational burden of different matching formulas

For businesses focused on hiring placement in competitive sales markets, the company match often represents a relatively cost-effective differentiator compared to increasing base salaries.

Company Match in Total Compensation Philosophy

The company match should integrate into a comprehensive total compensation strategy rather than existing as an isolated benefit. When building a sales team, employers must consider how retirement benefits complement base salary, commission structures, health insurance, and other perks.

High-performing sales professionals evaluate opportunities holistically. A lower base salary with generous company match, strong commission structure, and quality benefits may surpass a higher base salary with minimal additional compensation elements.

Communicating Value to Employees

Many employees underestimate the value of their company match, focusing primarily on take-home pay. Employers should regularly communicate the dollar value of matching contributions and their long-term impact.

Annual benefits statements that itemize employer contributions help employees appreciate total compensation. For a salesperson earning $100,000 with a $5,000 annual company match, health insurance valued at $15,000, and other benefits totaling $8,000, their true compensation exceeds $128,000-a significant difference from the stated salary alone.

Future Trends in Company Match Programs

The landscape of retirement benefits continues evolving. Some employers are experimenting with student loan matching programs, where companies make 401(k) contributions for employees who make student loan payments instead of traditional retirement contributions.

Kiplinger's analysis of 401(k) pros and cons highlights both the advantages of employer matches and potential limitations of 401(k) plans generally. As regulatory frameworks evolve and employee preferences shift, forward-thinking employers adapt their company match programs accordingly.

Younger employees entering the workforce, including those in remote appointment setter positions, may prioritize different benefit structures than previous generations. However, the fundamental appeal of "free money" through company matching remains universally attractive.

Integration with Broader Financial Wellness

Progressive employers increasingly view the company match as one component of comprehensive financial wellness programs. These programs might include financial planning resources, emergency savings accounts, health savings account matching, and educational resources about maximizing retirement benefits.

For businesses in the sales recruitment industry, understanding these trends helps position opportunities effectively and advise clients on competitive benefit structures that attract top performers.

Company Match and Business Growth

Establishing a company match program requires financial stability and predictable revenue. For high-growth businesses, particularly those in the coaching, consulting, or agency space selling services over $2,500, implementing matching contributions often coincides with business maturation.

The company match signals to employees, customers, and the market that a business has moved beyond startup phase into sustainable operations. This perception matters when recruiting experienced sales professionals who seek stability alongside opportunity.

Growth stage considerations:

Startup phase - Focus resources on growth; delay company match implementation

Growth phase - Introduce modest matching to compete for talent

Maturity phase - Expand matching generosity to retain institutional knowledge

Enterprise phase - Benchmark against industry leaders for competitive advantages

Business owners must balance investing in growth initiatives against providing employee benefits. However, the retention value of a company match often justifies the expense by reducing costly turnover and maintaining productivity.

Understanding company match programs and their strategic value enables both employers and employees to make informed decisions about retirement planning and total compensation. Whether you're evaluating benefits as an employee or designing competitive packages as an employer, the company match remains a cornerstone of modern compensation philosophy. If you're ready to build a high-performing sales team with professionals who appreciate comprehensive benefits and deliver exceptional results, Sales Match provides access to pre-vetted sales talent specifically for high-ticket businesses, with an unlimited replacement guarantee that ensures you always have the right people driving revenue.